The concept of financial inclusion has been around for quite some years under one or the other name and with one or the other focus area – micro finance, micro leasing, micro insurance, special programs for supporting women in business, special programs for supporting young entrepreneurs, programs for ensuring access to finance for the poor, etc.

But what does financial inclusion mean and why is financial inclusion so important?

The World Bank defines financial inclusion to ‘… mean that individuals and businesses have access to useful and affordable financial products and services that meet their needs – transactions, payments, savings, credit and insurance – delivered in a responsible and sustainable way.’ [1]

Having some form of ‘transaction account’ is a first step toward broader financial inclusion. A transaction account allows for people to keep money, to send and receive money in a safer, faster and more effective way than keeping cash under their pillows, running around with a bag of cash or asking someone else to transport cash for them.

Access to convenient, affordable and safe financial services saves time and effort and allows to use time and resources in more productive and efficient ways. Availability of such financial services also allows to do things that could not be done before, such as taking out an insurance policy for example.

Against this background, financial inclusion has been identified as enabler for a number of the United Nations (UN) Sustainable Development Goals. Among others, access to financial services can enhance the creation of employment and economic growth, the implementation of green technologies, the reduction of waste or the provision of better education.[2]

It is estimated that, globally, there still are 1.7 billion unbanked adults.[3] And, regarding small and medium-sized enterprises (SMEs), the Global Partnership for Financial Inclusion estimates that about half of 400 million SMEs still have unmet credit needs, i.e. 180 to 220 million SMEs. This credit demand totals USD 2.1 to USD 2.6 trillion.[4]

In short, effectively serving un(der)-banked population and SMEs contributes to enhancing development.

Serving the un(der)banked also presents huge business opportunities.

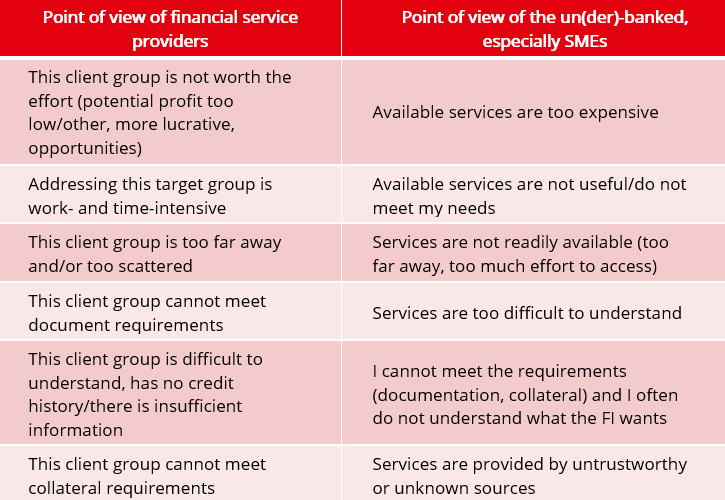

So, what stands in the way of financial inclusion?

Financial inclusion is hampered by a variety of factors. These include supply- and demand-side issues. The table below lists typical issues:

While the factors described above hamper financial inclusion in principle, they are especially relevant for SMEs because SMEs, due to their size and comparatively larger financing requirements, fall into a different category than consumers or micro businesses and (very) small enterprises (MSEs). Consumers and MSEs tend to be homogenous target groups. Like small-scale consumers, most MSEs are rather similar in profile and have similar needs. Therefore, it is comparatively easy to define a workable approach, procedures and products for these target groups and reach out to them on a broad basis, now leveraged by new technologies.

In this context, it should be noted that significant headway on financial inclusion in principle has been made in recent years, not least as a result of technical innovations which make out-reach and processing of vast amounts of data more feasible than in the past. At the forefront of this are new communication technologies such as smart phones and digital means of collecting, managing, processing and analysing large quantities of data. Globally, the number of the unbanked has decreased from 2 billion in 2011 to 1.7 billion in 2017. The share of adults with an account has increased from 51% to 69% between 2011 and 2017 (this includes mobile money accounts) and 54% of adults are considered financially resilient (i.e. could mobilise 1/20 of GNI p.c. within one month).[5]

New technologies as financial inclusion enablers

New technologies are obviously playing an important role in this rapid increase in inclusion. According to Findex, 65% of the 1.7 billion unbanked adults have a mobile phone and 25% have access to the internet and a mobile phone. Digital payments increased from 41% in 2014 to 52% in 2017 and the increase in digital payments is growing faster than the number of account owners.[6]

52% of adults, i.e. 76% of account owners made/received at least one digital payment in the past 12 months (44% of adults in developing economies) and mobile phone and internet coverage is noteworthy (Gallup World Poll 2017 based on Findex): in high income countries, 93% of adults have a mobile phone, 82% access to the internet and a mobile phone. For comparison, in developing countries, a noteworthy 79% have a mobile phone and 40% access to the internet and a mobile phone.[7]

New technologies allow to overcome some of the old issues and develop new business models. For example, the use of mobile phones makes distance and costs involved in serving a dispersed and low-volume-per-customer target segment not only feasible but also quite profitable. Use of ‘alternative credit scoring mechanisms‘ and ‘non-traditional information sources’ (e.g. data stored on mobile phones) for evaluating risk, supplemented by new technologies which allow for comparatively cheap data storage and processing of data, help resolve informational asymmetry and collateral issues usually associated with client groups with limited or no reliable data documentation.

As new technologies develop, new business models are developing.

Examples include:

- peer to peer (P2P) financing, i.e. debt financing from individuals for individuals (or small businesses) without the use of an official formal financial institution (FI) as intermediary; usually, an online service matches potential lenders and borrowers

- crowdfunding, i.e. small amounts of capital are collected from a large number of individuals and used to finance a (new) business venture using networks of people/websites to bring lender and borrower (investor and entrepreneur) together

- blockchain technology,e. using a digital ledger where transactions (in some cases relating to or in cryptocurrency) are recorded chronologically and publicly

- Smart contracts: i.e. self-executing contracts, where the terms of the agreement between buyer and seller are directly written into lines of code; the code and the agreements contained therein are available across a decentralised blockchain network; transactions are traceable, transparent and irreversible

- E-commerce platforms: i.e. a platform to allow for/manage commercial transactions conducted online

New technologies and new business models as panacea?

New technologies and new business models are playing an important role in enhancing financial inclusion. But, so far, most fintech lending models proved suitable for rather small amounts only, i.e. for consumer lending and very small businesses (micros) but not for larger amounts and the upper end of the SME segment. Furthermore, in practice not all models proved as sustainably successful as hoped for and resulted in high numbers of arrears/negative effect on the credit history of borrowing individuals or businesses, etc. (e.g. in Africa). A number of platforms have also gone ‘belly up’ (e.g. in China), i.e. ceased to exist due to mismanagement, fraudulent practices or hacking, for example in the case of platforms or blockchains. More importantly, however, is that many offers do not meet the actual needs of individuals and, especially, those of small businesses, i.e. standardised product offers often mean that amounts are either too small or too big to actually fit with what the business needs or that maturities are too short or too long, etc.

So, what about SMEs?

SMEs need comparatively larger amounts than consumers or MSEs. This in itself changes the risk profile and has consequences for the conditions at which financial service providers would be willing to provide financing. Often, SMEs need more individually tailored products than consumers or MSEs, so that a fully standardised approach and product-offer frequently does not match actual needs of SMEs. At the same time, many SMEs still share characteristics with MSEs when it comes to transparency, reliable documentation, documented assets and available collateral. This again has implications for the risk profile and the technology that can be meaningfully applied to assess creditworthiness of applying SMEs. SMEs tend to be diverse, i.e. not as homogenous as target group as the micro segment and low-end of the small segment. Consequently, technologies that can be successfully applied to consumers or MSEs often do not work for SMEs. And this seems to hold true for many of the new technologies and business models as well.

So far, cash flow-based lending, i.e. lending to SMEs based on ‘knowing the customer’, truly understanding actual cash flows, actual assets, profit, history and plans of a business seems the most robust and sustainable model – even if not the cheapest or easiest to implement. And, new technologies can most certainly assist in making this approach more attractive for FIs. New technologies can help in lowering costs related to data retrieval, storage and processing for example. They can also allow to lower costs related to serving clients and reaching out to SME clients on a broader basis.

However, some fundamental issues do not go away just by offering digital services or employing new business models. This includes issues related to lacking financial literacy/financial know-how of individuals and SMEs, unresolved consumer protection issues, other legal and regulatory short-comings, lacking know how of FIs in how to assess SMEs and offer financing tailored to the needs of SMEs as well as lacking availability of long-term finance, ideally in local currency, to be able to offer SMEs tailored (investment) finance. And this is where governments, international financial institutions (IFIs) and other international organisations come in.

The role of governments, IFIs and other organisations

There are conditions and requirements that need to be met to enhance MSME development in principle. And this includes creating the environment in which also new technologies and new business models can operate in a sustainable and effective manner while enhancing actual financial inclusion.

It is up to policy makers and law makers to create the necessary environment. Foremost, requirements and conditions needed for enhancing financial inclusion include:

- Regulation that permits for alternative financing but ensures consumer protection and financial stability

- Functioning credit bureaus/informational infrastructure to support credit risk assessment/store information on credit history/make credit history available

- Government support: public (ideally public-private) risk sharing mechanisms, e.g. guarantee schemes, public-private equity funds; financial literacy campaigns, etc.

IFIs and other organisations can play an important role by supporting governments in creating the needed environment to enhance financial inclusion of individuals and MSMEs by:

- Supporting policy makers and governments in creating the needed regulatory environment and risk sharing mechanisms

- Setting standards for Social Performance Management (SPM)

- Supporting establishment of functioning credit bureaus/informational infrastructure

- Supporting initiatives to enhance financial literacy

In addition, in particular IFIs, can play a crucial role in enhancing access to finance for SMEs by making long-term funding (ideally in local currency) for financing SMEs and technical assistance available to FIs to enhance the knowhow of institutions on how to tailor services to the needs of SMEs.

The Regional Small Business Programme (RSBP) in Mongolia as part of enhancing financial inclusion

The RSBP was created with support of the EBRD and the EU specially to enhance the know-how of FIs on how to serve MSMEs and to encourage the use of digital means (new technologies) in communication and training. More specifically, the RSBP offers (some) class room training and access to online information and training to FIs in Mongolia, with the goal of improving how FIs work with small businesses. By placing the main emphasis on developing the knowledge sharing and exchange platform (KSEP) and encouraging use of the platform, the RSBP is also contributing to the transition of FIs in Mongolia to use of new technologies.

In this way the RSBP contributes to enhancing financial inclusion of SMEs while also contributing to the up-take of new technologies by financial sectors in Mongolia.

[1] https://www.worldbank.org/en/topic/financialinclusion

[2] https://www.un.org/sustainabledevelopment/sustainable-development-goals/ The United Nations Sustainable Development Goals

[3] https://globalfindex.worldbank.org/

[4] https://www.gpfi.org/sites/default/files/documents/GPFI%20Report%20Alternative%20Data%20Transforming%20SME%20Finance.pdf

[5] GNI p.c. stands for Gross National Income per capita

[6] https://globalfindex.worldbank.org/

[7] https://news.gallup.com/opinion/gallup/235151/mobile-tech-spurs-financial-inclusion-developing-nations.aspx

Disclaimer

This document was published to contribute to and stimulate discussion on topics related to MSME finance or other related relevant topics in Central Asia. The views presented are those of the author/authors of this document, and do not necessarily represent the views of EBRD or contributors and donors of the RSBP for Central Asia. The RSBP for Central Asia does not guarantee the correctness, completeness or quality of the information provided in this document. The RSBP for Central Asia, its contributors and donors do not take any responsibility for any damage caused by the use of the information published in this document.